Traditional retirement systems are struggling to keep up with the realities of modern life. People are living longer, costs are rising, and savings are not keeping pace. According to the World Economic Forum (2024), these challenges threaten the financial security and dignity of aging populations worldwide. As leaders seek innovative solutions, artificial intelligence (AI) has emerged not just as a tool for optimization, but as a potential cornerstone for a new retirement paradigm—one that is smarter, more inclusive, and digitally empowered.

This article was optimized by the PublicistBot.

Want 10 articles per month promoting your business & making you money on autopilot? Activate the PublicistBot for $299.99/year. Add 720 short-form videos for $250 per month more.

Learn More About the Offer in This Article

Send your interest to the appropriate article or offer owner. PMN records the article that generated the enquiry, updates the funnel, logs the activity, sends notifications and adds the lead to PMN Messages.

The exact article is saved with the lead.

The featured offer or redemption link is preserved.

Owners receive messages and email notifications.

The applicant is connected to the campaign source.

This article builds on research from the World Economic Forum, Mercer, and the OECD to explore how AI and new platforms like SAHOP (Standalone Hands-Off Program), the EventBot, and the Social Rewards system can support the next generation of retirees.

The Problem: Retirement Models in Crisis

| Metric | Statistic | Source |

|---|---|---|

| People with inadequate retirement savings | 45% of global workforce at risk | World Economic Forum (2024) |

| Employees who feel confident about savings | Only 45% | Mercer Global Talent Trends 2024 |

| Life expectancy extension | +20 years beyond retirement age | OECD (2024) |

| Employers who prioritize retirement benefits | Just 38% | Mercer Global Talent Trends 2024 |

AI's Contribution to a Retirement Renaissance

1. Redefining Adequacy Through Personalization

Retirement adequacy refers to whether current systems can provide enough income for retirees. Six key design features determine this adequacy, and AI can improve all of them:

| Feature | How AI Helps |

| Tax Incentive Optimization | Forecasts ideal contribution levels and tax benefits |

| Benefit Preservation | Predicts risk of early withdrawals and nudges users to retain savings |

| Vesting/Portability | Analyzes employment trends to suggest flexible plan options |

| Benefit Design | Recommends custom payout mixes (lump sum vs. annuity) |

| Life Event Response | Models fair benefit divisions during divorce or medical leave |

| Accrual Support | Identifies ways to continue accruing benefits during unemployment |

Platforms like SAHOP automate this personalization through data-driven onboarding and AI-powered learning paths, ensuring each retiree receives recommendations tailored to their career, income, health status, and life goals.

2. Sustainability: Enabling Longer Workforce Participation

The old-age dependency ratio is rising, placing pressure on pension funds. AI can ease this strain by:

-

Identifying phased retirement options for older workers

-

Recommending skills training to extend digital employability

-

Matching older workers to flexible job opportunities

-

Analyzing contributions vs. outflows to adjust plan rules dynamically

The EventBot complements this by automating income generation through webinars, podcasting, affiliate programs, and digital content monetization—creating revenue streams for retirees without physical labor.

3. Integrity and Trust in an Automated Future

Retirement systems thrive only if users trust them. AI can:

Turn one article into an ongoing visibility engine.

PublicistBot can keep your business visible with monthly articles, search-friendly distribution, affiliate-aware sharing, and optional AI Marketer video content.

Learn How to Share This Article and Earn $1.00 per Free Enquiry

Ask PMN how referral-aware article sharing works, how eligible free enquiries are attributed, and how Social Rewards are tracked in your account.

The exact article is saved with the lead.

The featured offer or redemption link is preserved.

Owners receive messages and email notifications.

The applicant is connected to the campaign source.

-

Simplify and standardize plan communications

-

Automate administrative compliance and cost-reduction

-

Use generative AI to create educational content that explains investment risk and benefits

The Social Rewards platform ensures that trust is tied to value. It offers:

-

$1.00 or more per qualified lead

-

Crypto, credits, or cash for digital engagement

-

Transparent affiliate tracking for all earnings

This transforms passive beneficiaries into empowered participants in their financial journey.

4. Smarter Investment Outcomes with AI

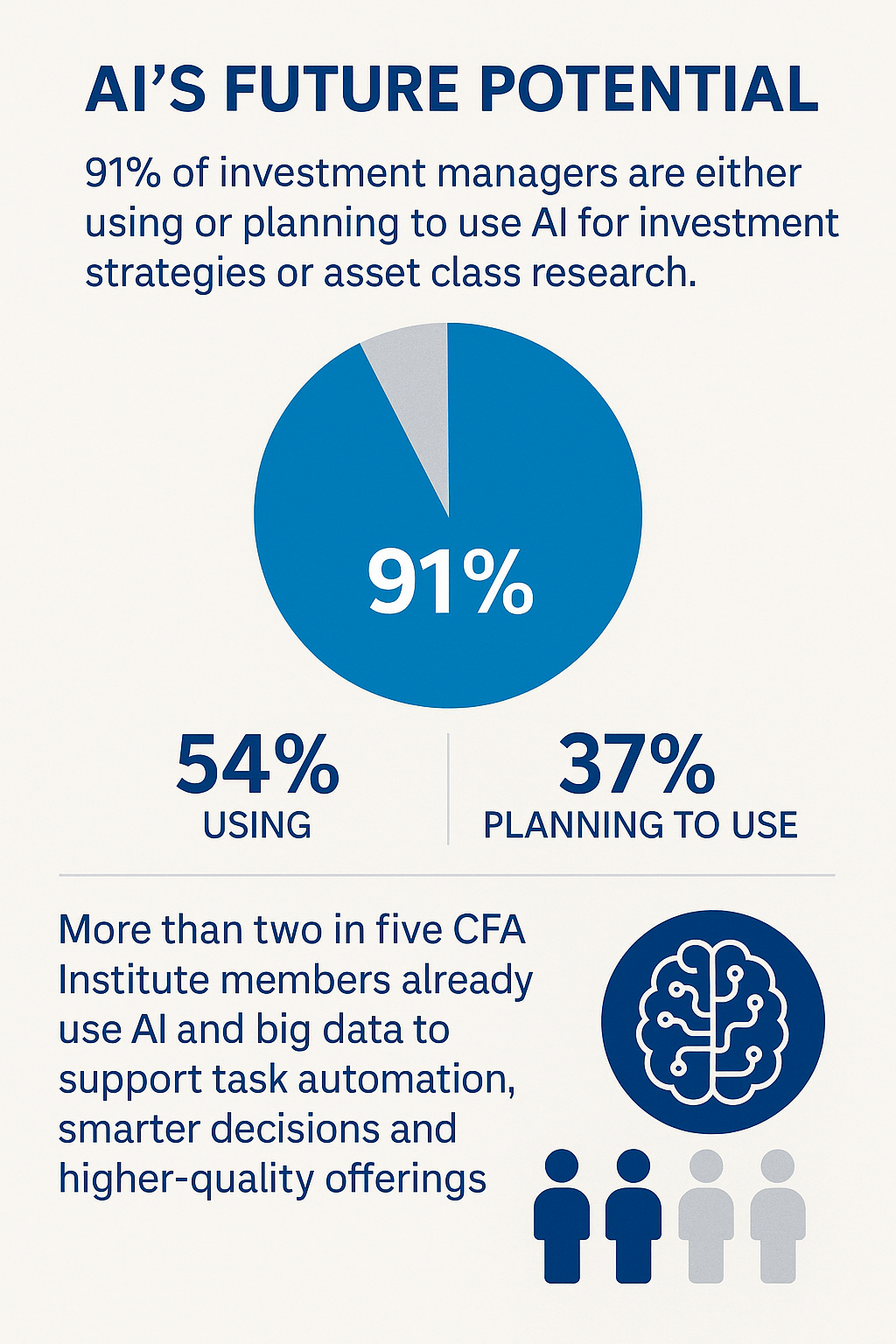

According to Mercer, 91% of investment professionals already use or plan to use AI to:

-

Analyze market signals for risk-adjusted returns

-

Detect hidden correlations in economic data

-

Predict member behavior for cashflow modeling

-

Optimize portfolio allocations for social impact

By integrating the EventBot and SAHOP, retirees can benefit from these high-performance investment strategies without needing financial expertise.

5. Bringing Financial Wellness into the Workplace

Workers need help navigating retirement decisions from the moment they enter the workforce. Yet many are underserved:

-

Only 18% of employers understand workers' retirement adequacy

-

72% of employees in the U.S. expect their employer to help with retirement planning (Mercer, 2024)

AI can change this:

-

Predicts retirement readiness based on behavior

-

Recommends personalized benefits using real-time data

-

Crafts tailored education paths for saving, investing, and goal setting

Platforms like SAHOP democratize this access by offering plug-and-play modules for employers and self-employed workers alike.

The Retirement Revolution Will Be Automated

AI alone won’t solve the retirement crisis. But combined with ethical oversight, digital education, and participation incentives, it can shift retirement from a place of fear to one of empowerment.

SAHOP, the EventBot, and Social Rewards aren’t just tools—they are the architecture for a more inclusive, resilient, and intelligent financial future.

References

-

World Economic Forum. Longevity Economy Principles, 2024. https://www.weforum.org/publications/longevity-economy-principles-the-foundation-for-a-financially-resilient-future/

-

Nazeri H. “People are living longer. So how can we build resilient economies?” https://www.weforum.org/agenda/2024/01/longevity-economy-thriving-societies/

-

OECD. Old-age dependency ratio, 2024. https://www.oecd.org/en/data/indicators/old-age-dependency-ratio.html

-

World Economic Forum. Global Risks Report, 2024. https://www.weforum.org/publications/global-risks-report-2024/

-

Whiting K. “We’re living longer. Here’s how that will change retirement,” 2023. https://www.weforum.org/publications/global-risks-report-2024/

-

Mercer. Global Talent Trends Report, 2024.

-

Mercer CFA Institute. Global Pension Index, 2024. https://www.mercer.com/insights/investments/market-outlook-and-trends/chasing-brighter-futures-ai-and-retirement-plans/

Want more optimized articles like this?

PMN can create and promote up to 120 PublicistBot articles per year for $299.99/year, with an optional AI Marketer video add-on that adds up to 720 videos for $250 per month more.

Learn How to Earn $90.00 When a User Activates PublicistBot AI Agents

Ask PMN about the PublicistBot referral process, eligibility, attribution, commission tracking and the steps required for a qualifying activation.

The exact article is saved with the lead.

The featured offer or redemption link is preserved.

Owners receive messages and email notifications.

The applicant is connected to the campaign source.